Fundraising dynamics

The VC ecosystem in Europe has been navigating through a complex and evolving fundraising environment, shaped significantly by the reverberations of the tech reset. The year 2023 offered a telling cross-section of this dynamic, with fundraising activities reflecting broader economic sentiments and strategic shifts within the industry.

The 2023 fundraising landscape

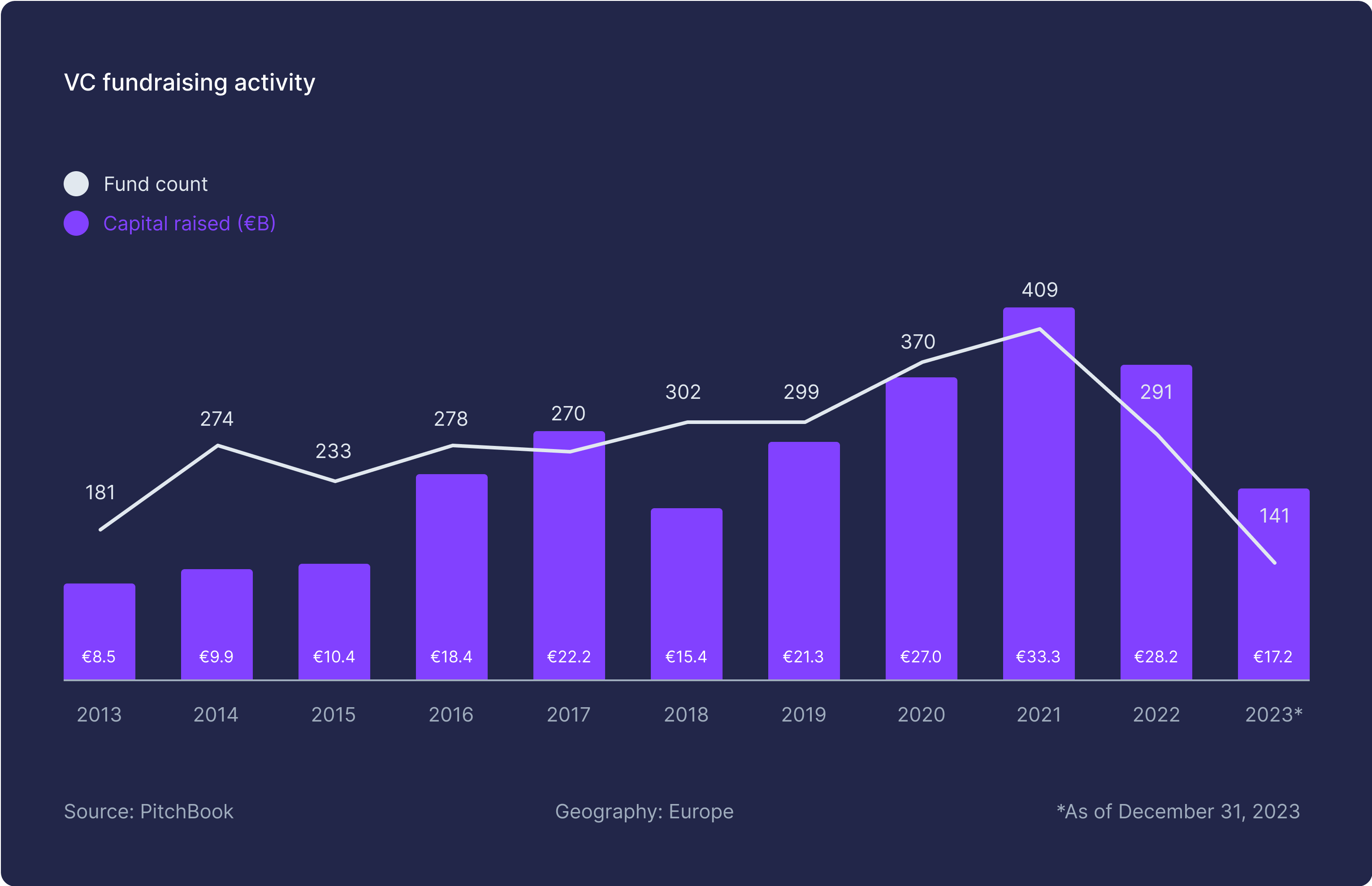

The aftermath of the tech reset has been palpable across European VC fundraising, which experienced a considerable contraction in 2023. Statistics point to a total of €17.2 billion raised over 141 funds, which indicates a stark 39.0% decline in the capital amassed compared to the preceding year, accompanied by a 51.5% decrease in the number of funds. The data underscores a more cautious approach from LPs and GPs, a trend attributed to a recalibration following market exuberance and a heightened focus on sustainable investments.

Experienced vs. emerging firms

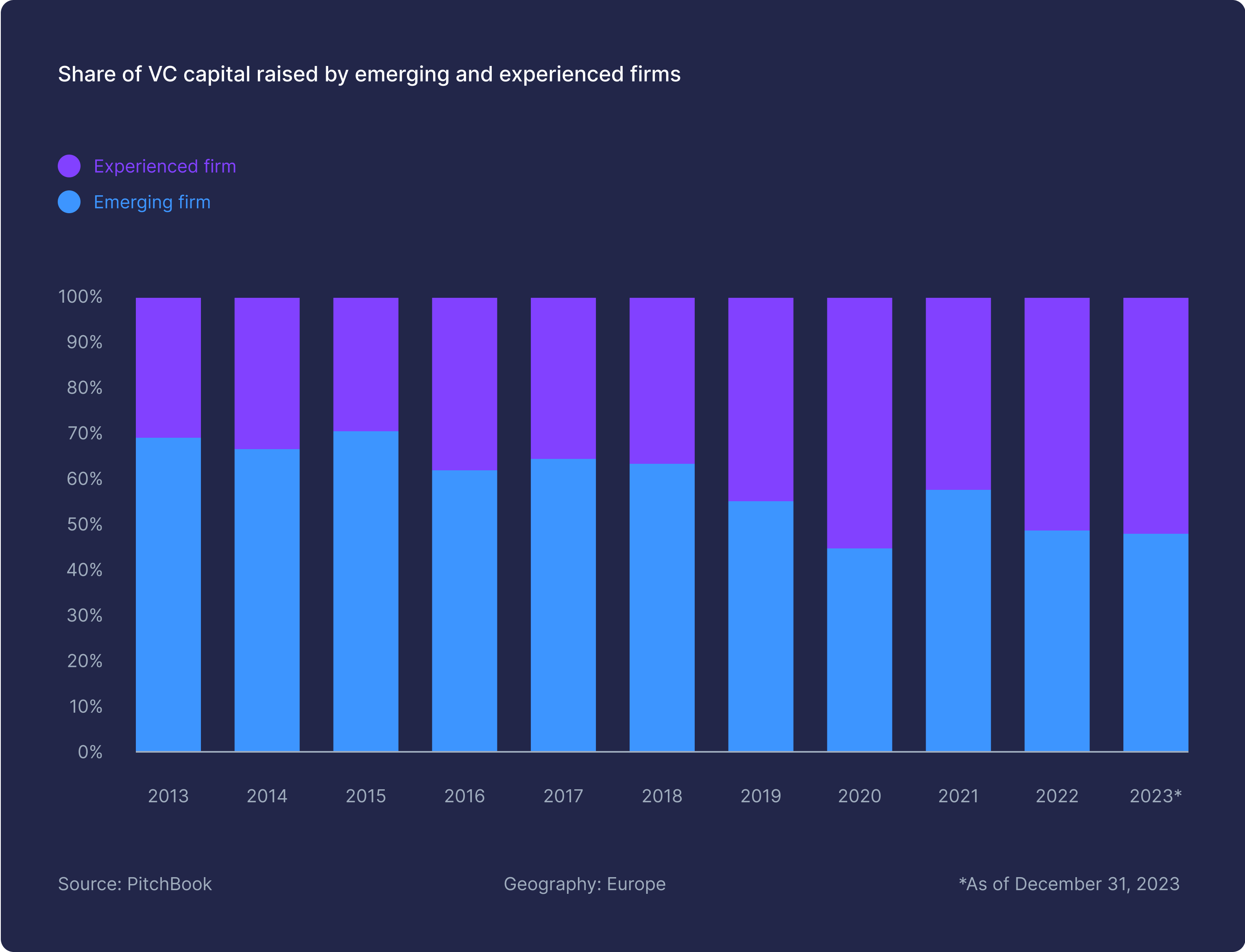

The fundraising climate favoured experienced firms, which captured 54.5% of the total capital raised in Europe for the year. Amidst a challenging market backdrop and subdued returns, LPs showed a marked preference for established funds with a track record of performance.

As a result, emerging managers suddenly faced increased competition from well-established firms. These established firms, unable to rely solely on their existing relationships, were now compelled to seek out new investors. From the LP perspective, this was a golden opportunity to start building relationships with the top tier firms they had not been able to access during the bull run. The combination of both giving (at least the perception of) a safer harbour and the ability to start building relationships with the most sought-after managers did not make the raise easier for new managers.

The ascendancy of larger funds

Within this cautious fundraising milieu, 2023 observed a noteworthy migration towards the formation of larger funds. Evidently, the funds that crossed the €500 million threshold represented 28.4% of the total capital raised. This near-doubling of their previous year’s share is significant, reflecting a strategic consolidation of capital into larger, presumably more stable vehicles. Such funds, as typified by the massive raises by firms like Speedinvest, Highland Europe and HV Capital, became the flag bearers of this shift, signifying a preference for scale and a penchant for backing established platforms that promise resilience and growth potential amidst the prevailing uncertainties.

The trajectory of this fundraising landscape, with its pivot towards larger funds, appears to be a direct consequence of the tech reset. Investors and fund managers are prioritising robustness and a reduced appetite for risk, likely envisioning these substantial funds as safe harbours in the choppy waters of a post-reset marketplace. As we delve deeper into the analysis, it will be imperative to consider how this trend is influencing investment theses, operational models, and the overarching strategies employed by VC players in the European context.

Case study: Raising €500 millions with Speedinvest

We sat down with Daniel Keiper-Knorr, founding partner of Speedinvest, for a discussion on what he thinks allowed them to raise €500 millions during and after the tech reset.

What ensued was a conversation revealing how Speedinvest decided to diverge from traditional VC practices by dedicating substantial resources, including the full time attention of Daniel, one of the founding partners, to fundraising and investor relations.

Key learnings

Economic sensitivity and its implications for venture capital

One of the most striking revelations from Daniel’s experience is the profound impact of global economic conditions on venture capital dynamics. He delves into how the sudden shift in LP inquiries from portfolio-centric to macroeconomic concerns mirrored the broader economic uncertainties, highlighting the necessity for VCs to be economically astute. This sensitivity to macroeconomic shifts is not just about staying informed but about integrating this understanding into the strategic narrative of the fund. Daniel’s recount of adapting Speedinvest’s narrative in response to changing economic sentiments underscores the importance of this adaptability not as a reactionary measure but as a strategic imperative. It serves as a compelling reminder that venture capital, while focused on the future, must navigate the present’s economic realities.

The art and science of LP communication

Daniel’s emphasis on transparent and ongoing communication with LPs underscores a fundamental pillar of successful venture capital operations. The strategic approach to communication — viewed through the lens of building trust and managing expectations — is both an art and a science. Daniel illustrates how Speedinvest’s preemptive communication strategy, especially in times of strategic pivots or market volatility, has been instrumental in reinforcing trust with LPs. This proactive engagement goes beyond regular updates, encompassing a nuanced understanding of LP preferences and concerns and the strategic dissemination of information to mitigate surprises and align expectations. It’s a testament to the view that, in the realm of venture capital, effective communication is as crucial as financial acumen.

Navigating shifts with agility and insight

The conversation further illuminates the critical importance of agility in the face of market shifts. Daniel’s narrative brings to life the concept of strategic adaptability, not just as a response to changing market conditions but as a proactive stance in anticipation of these changes. This agility, underpinned by a thorough understanding of both the venture ecosystem and broader economic indicators, is pivotal for the relevance and efficacy of venture funds in fluctuating times. It’s about the capacity to pivot not just in strategy but in the narrative, ensuring that the fund remains aligned with the evolving priorities and concerns of investors.

Leverage experience in winning confidence

Speedinvest’s journey through various economic cycles, as narrated by Daniel, accentuates the invaluable role of experience in the venture capital landscape. This seasoned expertise, characterised by a history of navigating booms and busts, is a cornerstone in building and sustaining LP confidence, particularly during turbulent market conditions. Daniel’s reflection on Speedinvest’s strategic decisions, underpinned by decades of collective experience, underscores the trust that experience engenders in investors. It’s a poignant reminder of the weight that history and track record carry in the venture capital arena.

The strategic importance of local markets

Finally, Daniel’s insights on the significance of local markets in Speedinvest’s fundraising success story offer a compelling perspective on the value of nurturing local investor relationships. Despite the allure of global expansion, the substantial support from within Austria highlights the untapped potential and strategic importance of home markets. This aspect of Speedinvest’s strategy underlines a broader lesson for the venture capital community: the power of local ecosystems as a bedrock for support and growth. It challenges the venture capital ethos to look beyond the global horizon and recognise the value lying within their immediate geographical and economic contexts.

Case study: Raising €780 millions with HV Capital

In our conversation with Rainer Märkle from HV Capital, we explored the strategies and insights behind their successful fundraise amidst the fluctuating European venture capital scene. HV Capital’s transition from a corporate venture entity to an independent powerhouse presents a narrative of strategic adaptation, insightful investment diversification, and the importance of solid relationships with investors.

Rainer opened up about the journey of becoming independent, the rationale behind their diversified investment approach, and the significance of nurturing long-term partnerships with LPs. He also shared how they stayed focused through market uncertainties and the role emerging technologies like deep tech play in their strategy.

Here’s what we took away from our talk with Rainer:

Key learnings

Strategic independence and evolution

Rainer highlighted the transition from a corporate venture arm to an independent venture capital firm. This wasn’t a mere change of status but a strategic evolution driven by the desire to capitalise on broader opportunities that the confines of a corporate structure could not accommodate. The move to independence was underpinned by a vision to fully engage with the dynamic venture ecosystem, reflecting deep strategic foresight. It’s about identifying when the protective corporate umbrella no longer serves growth but hinders potential, a nuanced insight for GPs contemplating similar shifts.

Tailored dual fund strategy

HV Capital’s approach of operating two parallel funds dedicated to different growth stages is not just a diversification tactic but a nuanced strategy to address specific market needs and opportunities. This dual-fund approach allowed HV Capital to tailor its strategies, management, and resources to the unique demands of early-stage ventures versus more mature, growth-stage companies. Rainer’s explanation sheds light on the thoughtful segmentation of investment strategies, emphasising the importance of specificity and focus within each fund to effectively meet the objectives and expectations of different investor bases.

The art of LP relationship management

Rainer’s discussion on LP relationships extends beyond the typical advice of keeping investors informed. It delves into the art of building trust through consistency and transparency, underpinned by a commitment to long-term partnerships rather than transactional interactions. The early commitments from their existing investor base, crucial for their recent fundraise, were not just a testament to past performance but a reflection of deeply nurtured trust and shared strategic vision. This underscores a sophisticated method of engaging with LPs, emphasising the importance of continuous dialogue, transparency in performance, and maintaining strategic consistency.

Navigating market volatility with strategic resilience

The recount of fundraising during a market downturn revealed the intricacies of decision-making in volatile environments. HV Capital’s experience underscores the delicate balance between adaptability to market conditions and steadfastness towards strategic goals. This balance is crucial in maintaining investor confidence and ensuring the fund’s strategic direction remains clear, even in uncertainty. Rainer’s insight into staying the course, despite market fluctuations, emphasises the nuanced understanding of market dynamics and investor psychology required for successful fundraising.

Embracing innovation with a forward-thinking investment focus

Rainer’s emphasis on deep tech and emerging sectors as key areas of focus for HV Capital goes beyond a simple endorsement of innovation. It reflects a strategic recognition of the transformative potential of these sectors, not just for the fund but for the broader market landscape. This approach showcases a sophisticated comprehension of technological evolution and its ramifications for future investment success. By prioritising sectors like deep tech, HV Capital positions itself not just as a participant in the venture ecosystem but as a forward-thinking leader anticipating and shaping future trends.

Case study: The evolution of fund sizes in European early stage

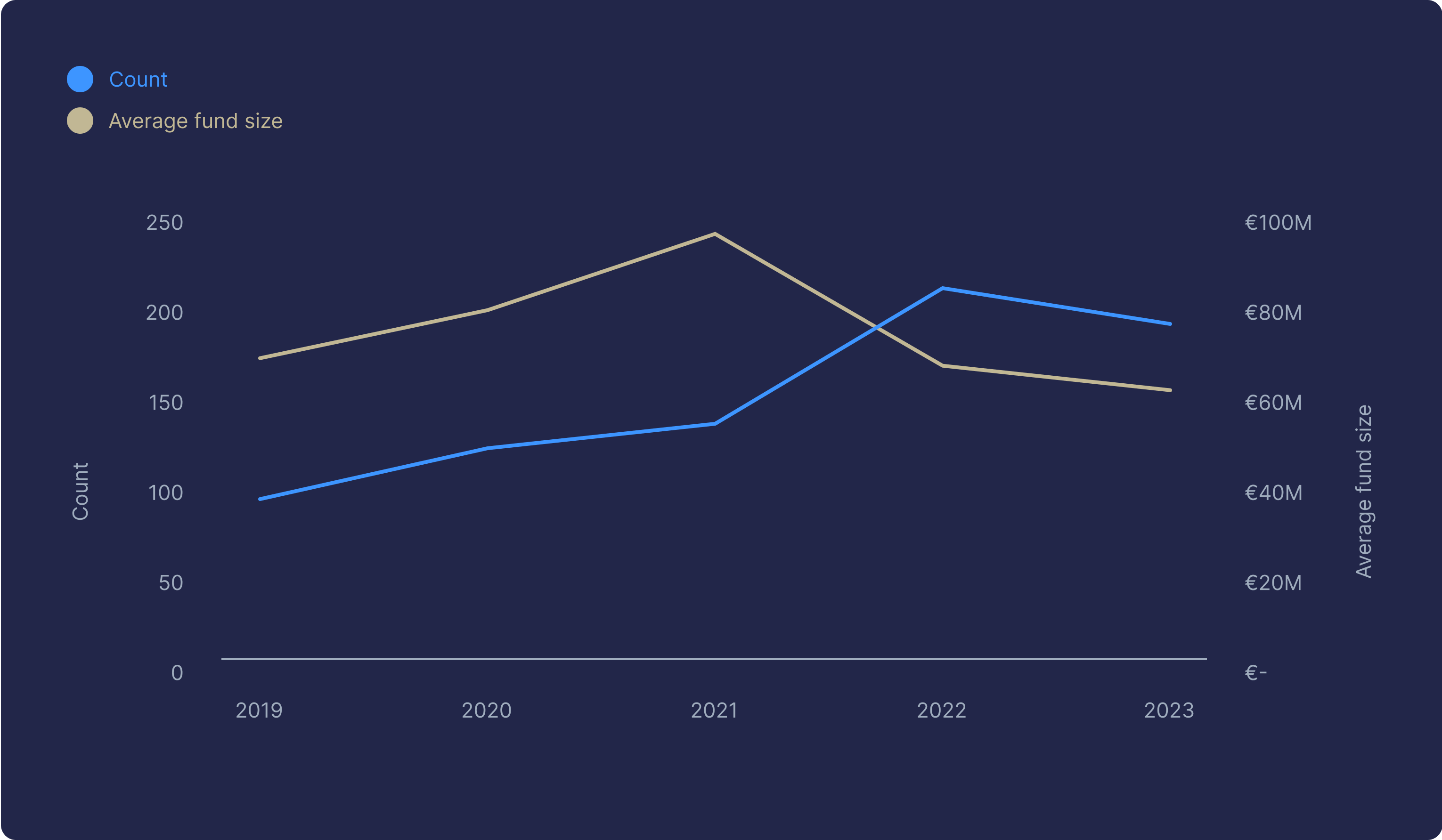

We dug into Isomer Capital’s data to demonstrate how the pipeline of one of Europe’s leading VC fund of funds changed over the period. While of course not market covering, it is an interesting perspective as they are the most active private market early stage VC fund of funds, with 4,000 funds screened, 1,611 VC firms actively tracked and 74 fund investments made leading to an underlying portfolio of over 2,000 companies.

The tech reset caused a significant drop in the average fund size in the Isomer pipeline from a high in 2021 of €95 million to €65m in 2022 and €60m in 2023.

This downsizing in fund size is likely a manoeuvre by managers to maintain agility and minimise exposure amidst market uncertainty and valuation corrections. Notably and in correlation with the lower impact of the tech reset on funding conditions for established managers, this is a trend we most predominantly see with emerging managers and micro funds (which make up a substantial part of the data set as Isomer has built a separate allocation to back these).

Interestingly, 2022 had the highest quantum of early-stage VC funds tracked by Isomer which is an expression of Isomer Capital’s continued growth and coverage more than the market. Invest Europe data shows that 2021 was the peak year with 383 funds raised versus 343 in 2022.

To take a closer look at emerging managers, we analysed the average number of early stage funds tracked by Isomer. The figure was calculated using the sum of fund numbers (ie Fund II = 2) divided by the total fund count to indicate the state of emerging managers. The 2021 vintage year saw the average fund raised was Fund 2.0, while in 2022 this number dropped to an average of Fund 1.7, indicative of a rise in emerging funds. Diving deeper into 2022, Isomer saw a total of 120 Fund I’s launches (>50% of the early-stage funds tracked internally) at an average size of €45m, slightly below the €65m average in the year.

Consequently, the Isomer pipeline data suggests clearly that fund sizes for early stage firms in Europe shrunk as a consequence of the tech reset.

Below, we’ve assembled some of our best conversations from the eu.vc pod on fund sizing. Dive in.

So over the course of the 15 years that we’ve been operating, we now have five funds that we’ve raised. And just so that you can sort of understand how the funds grew, the first one was €2.5 million. The second one was €5 million. Third, almost €20 million. The fourth was €60 million. And the current one is €78 million. So they’ve been, to some extent, incremental. If you look at that, they sound incremental by today’s standards. But you have to rewind the clock and remember that when we were raising for our third fund, it was €20 million and our previous one was a €5 million fund. People saw that as a 4x increase in fund size. I mean, it was incomprehensible! It was like: Wow! you know? When we raised our €5 million fund, it was a 2x increase from our previous fund. So I think sometimes it’s relative, right?

This is our fourth fund, which is €75 million. The first one was in 2011 for €18 million. The second one in 2015 was €53 million. And that was because the EIF came in at the last minute and significantly increased the size. And then a third fund to continue that trajectory.

Back in 2018, we raised €100 million and that was from a realisation that in our second fund we potentially hadn’t kept as much capital as we wanted to have had for follow-ons, because defending your equity or even building it up in those following rounds can drive a lot of your returns. So we’re like, “Alright, this time, €100 million and we’re going to do 60% for follow on and 40% for new investments.”

Fast forward, I think the market heated up so much in 2020–2021 that we were basically not finding ourselves doing follow-ons as much as we could. So now, when we were fundraising for the fourth fund, we said, “Alright, let’s just rethink this back to where things were,” and that was the main reason behind raising €75 million instead of €100 million.

Funnily enough, the market has now changed again, where it’s cooled down significantly, and I think there’s going to be quite a bit of follow on or even bridge requirements. So you do want to keep quite a bit of capital for supporting the portfolio, but we’re still quite happy about the fund size because it gives us a lot of flexibility.

After the final closing, I decided to give it a first go for a deck for a potential Fund II. So I was thinking exactly about this question and what I noticed was that with Fund I, we reached market fit.

We created a new category called category leaders. We also have a super strong portfolio from our angel investments and a well-known brand.

And despite the several imitators that we have in traditional funds becoming gradually more diverse, the market opportunity is still super strong. So basically, having the strategy that we have right now is really good. And we were thinking about what could be a good fund size and the reasoning behind it is that, as I’m going to tell you, the first idea that we have is making it 50 million.

The reasoning behind that is just to make it relevant for the big institutional and governmental LPs and not too big so that we can still have our co-investment strategy, because we don’t want to be fighting over the percentages in the deals and we still want to be the ones that one can still have as a tag-along.

So what we’re actually looking at is maybe a slightly higher allocation ownership-wise, sometimes also being able to do co-leads, which is the part where we struggle with right now, and then having more capital available for other follow on investments, and an option to also go into slightly larger rounds and be a little bit more flexible, basically

I would say that a fund size below €40 or even €50 million is hard to support for us because the metrics just do not work. We have a large range of fund sizes, from €40-50 million to billions. And we are usually investing a minimum ticket of around €10 million. We can go much higher, but it’s not that common. I would say the sweet spot is around €20-25 million.

We are saying fund size is your strategy, but it also matters what region you are in. If there’s less follow-on funding, you need to be in control of your destiny.

As for the size, why €40 million? We went the hard route. We obsessed over this for a few months, trying to answer the question of what’s the right strategy and how to build it, and came back to the obvious answer. When you look at the people who do this type of business in other markets, these are the fund sizes. Everybody ends up with between €30 and €60 million.

But we will not reinvest in the current state of things because we really want to first focus on deploying on 30 companies, which is really what we’ve sold as a value proposition to our LPs.

Register to read more

Please fill in the form to access the full report.