Fundraising across Europe

The distribution of venture capital across Europe reveals insights into the maturity and dynamics of various ecosystems. In this section, we dive into the geographic dispersion of venture capital funds, break down Isomer Capital’s pipeline from a geographic perspective, explore how a fund of funds thinks about geographic coverage and dig into a region prior to investing there.

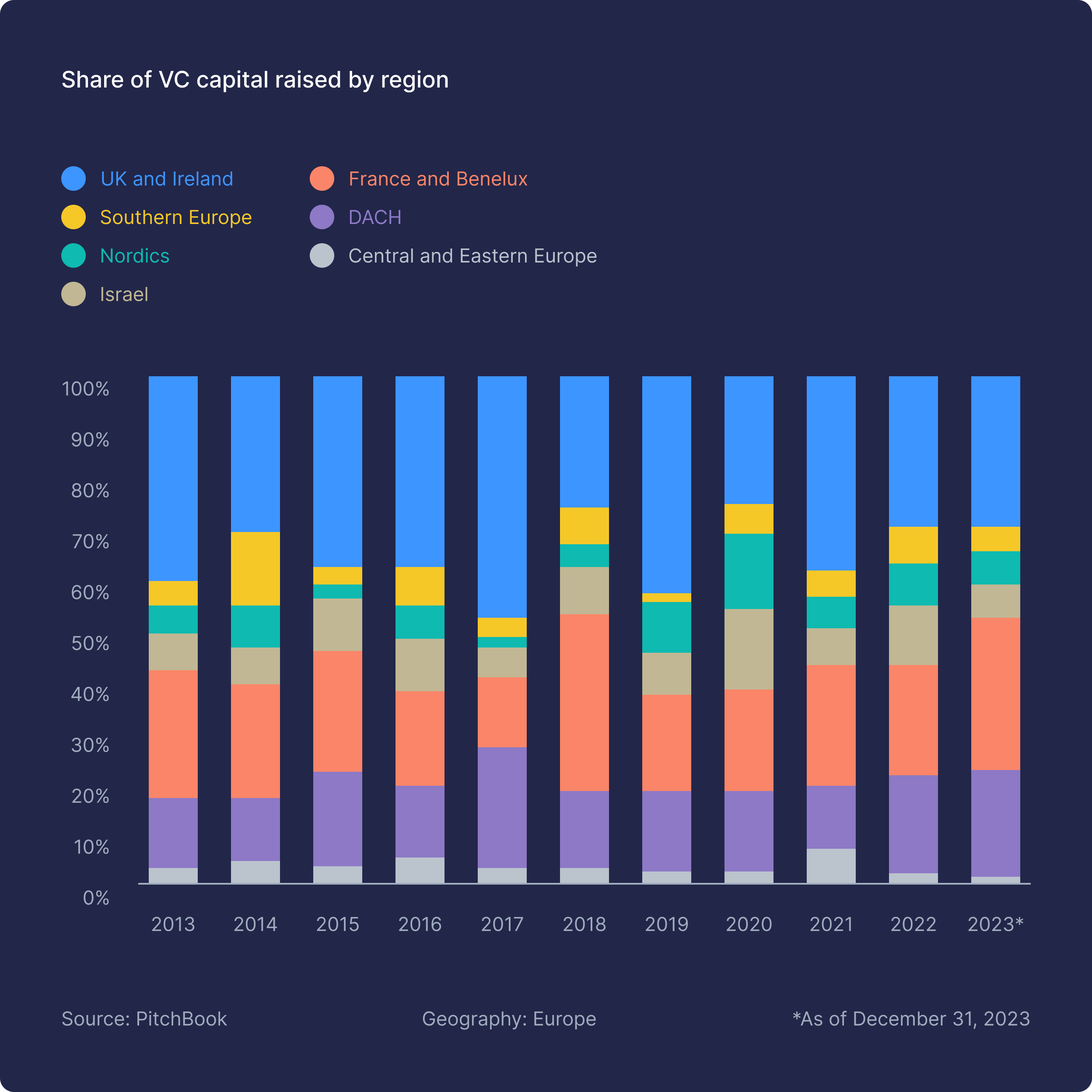

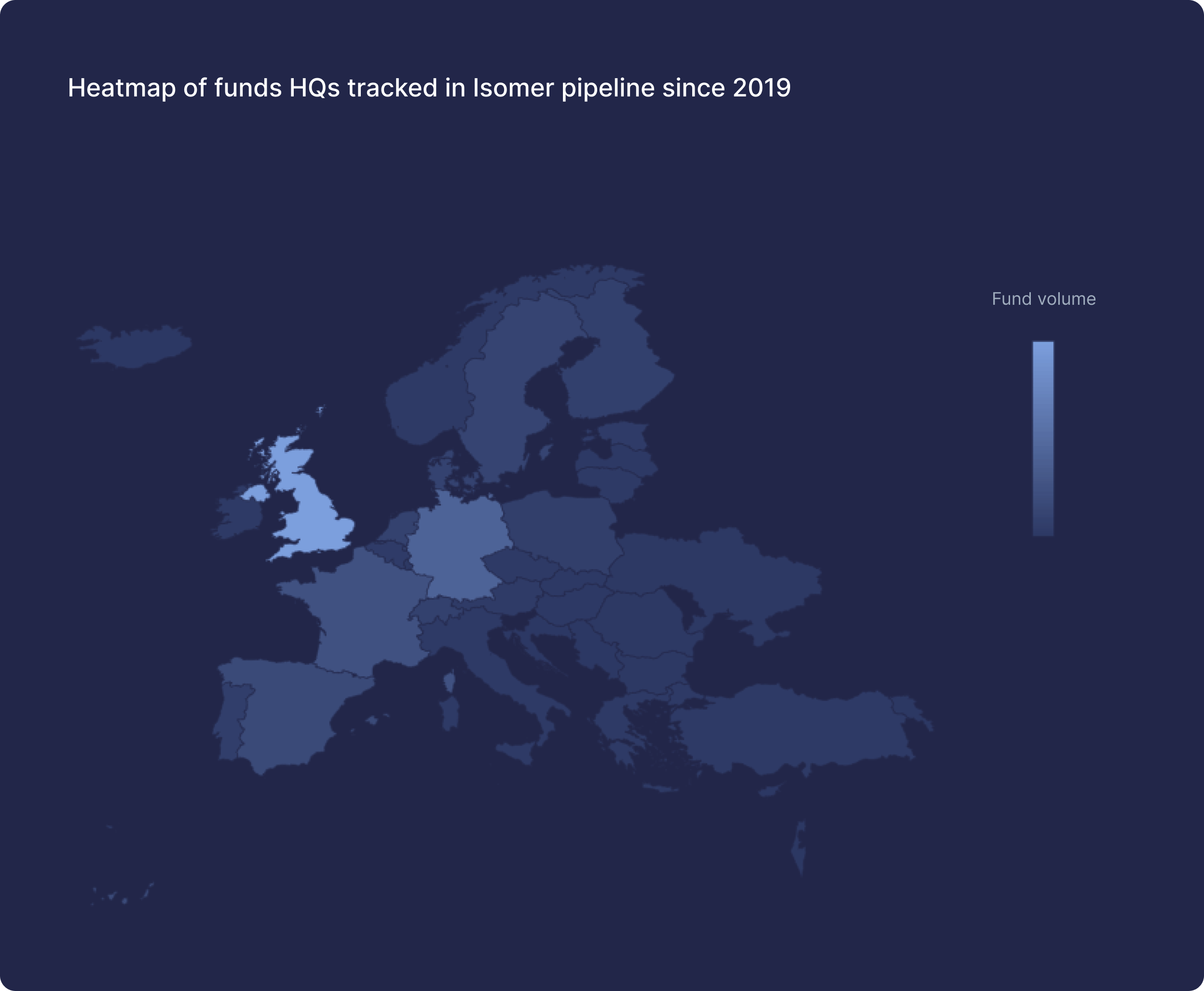

According to Pitchbook data, France and Benelux demonstrated robust resilience, with a mere 16.1% YoY decrease in capital raised. This performance brought the region’s share of total capital to 29.3%, placing it on equal footing with the historically dominant UK and Ireland, which maintained a 29.8% share. The DACH region also showed steadfastness, comprising 21.5% of the European market, signalling sustained investor confidence in these markets. This distribution is also reflected in the heatmap of Isomer’s fund pipeline below.

As European markets evolve, there has been a noticeable shift from local specialist funds to a broader cross-border investment approach. This trend is most prevalent in saturated and mature markets where venture capital is abundant. The more developed markets of the UK, France and Germany continue to contain the majority of funds raised in Europe. Outside of these geographies, there are notable and growing regions with a good amount of funds. Spain, for example, has continued to produce 8-10 early-stage VC funds a year for the last 5 years.

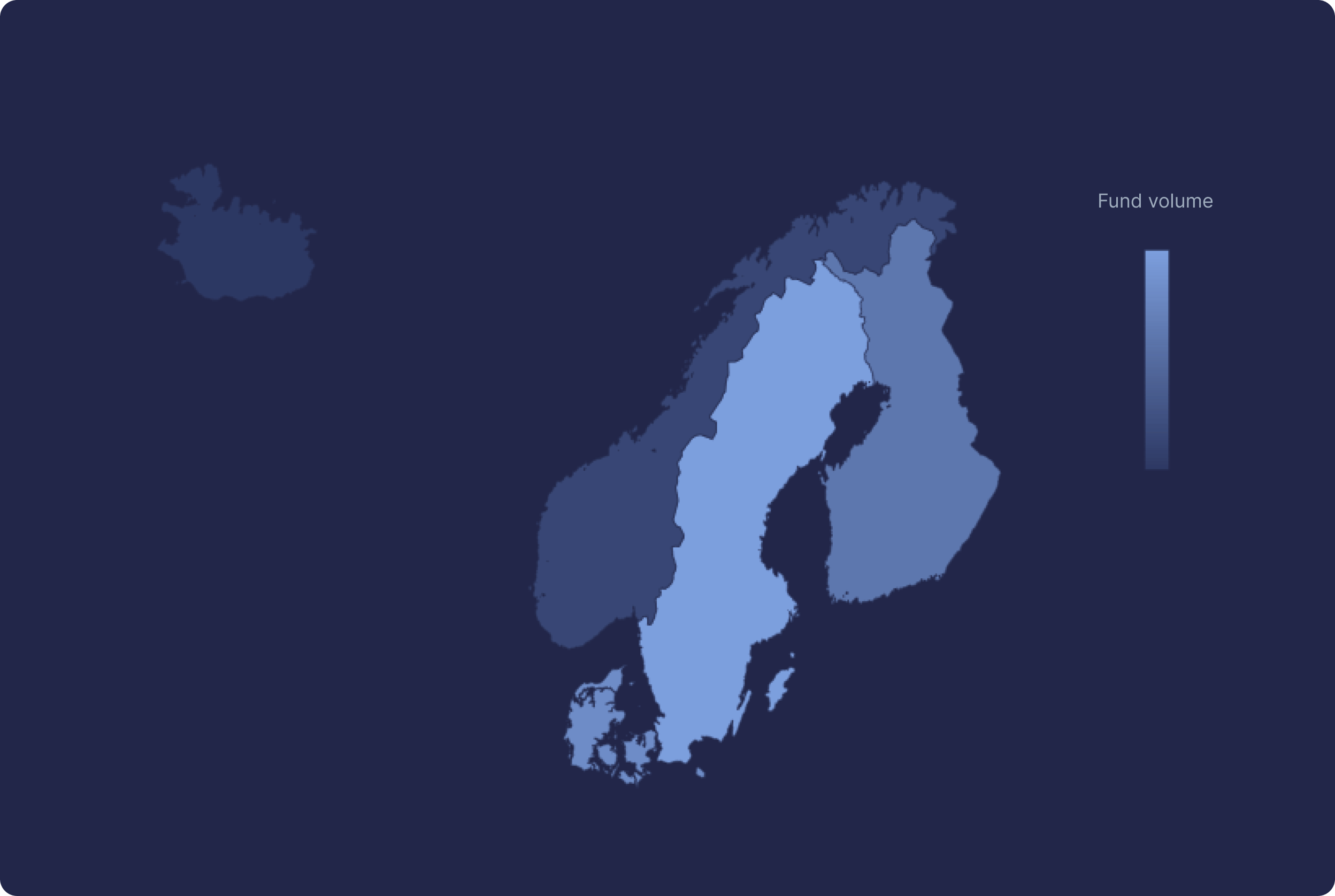

Historically, the Nordics have exemplified this localised investment climate with a higher propensity for domestic funding rather than pan-European engagement. Sweden, well known for its high unicorn production, has a high density of funds focused solely on the local market. Spinning out over 40 unicorns over the past few decades, it is easy to see why. However, things are evolving, Isomer’s Nordic deep dive (expanded on in the next section) illustrates how fund managers are creeping into pan-Nordic and beyond strategies. Cross-border investment is now becoming the norm.

Venture capital is not a national sport. It’s a global sport. We build amazing companies in Europe because we’re all from relatively small home markets and we have to build our companies outside of Europe and in the rest of the world. And we see companies starting in Sweden, then coming to London, then going to the US, or going directly to the US. This is a movable thing. So I get really frustrated when you hear politicians saying, “We are going to build the European Silicon Valley of X. That can, of course, have its place, but when we build the next generation of global leaders, they will have probably moved several locations before they end up IPO’ing in some marvellous way, and the way VC funds are built and invested has to reflect that”.

How LPs analyse a region before investing

Investment partnerships are initiated based on how well a manager aligns with an allocator’s strategy, rather than the allocator adjusting to the manager’s approach. Frequently, managers view the landscape solely from their own vantage point, overlooking the critical impact that dynamics on the opposite side have on securing a new investment.

In the following, we’ll digest Isomer Capital’s playbook for analysing a region before committing to new funds in it.

Isomer Capital’s approach not only encompasses rigorous filtering and evaluation but also a commitment to strategic investment principles and partnership synergies. Watch the full video to hear it from the team or read the key learnings for the big overview.

Key learnings

Initial fund pool and preliminary filtering

Isomer starts with an expansive view; in the case of the Nordics, they identified approximately 90 funds that could potentially align with their investment focus. The initial filtering phase is critical, setting the stage for a more in-depth analysis of the sector and stage fit.

Application of core fit criteria

The meticulous application of three core pillars—returns, diversification, and partnership—serves as the backbone of Isomer’s selection process:

- Returns-pillar: This pillar is central to the evaluation process, where a fund’s potential to deliver outstanding returns is scrutinised. This involves a deep dive into:

- The fund’s unique competitive edge and how it positions itself in the market.

- The composition and capability of the team managing the fund.

- The clarity and innovation within the fund’s investment thesis and strategy.

- Critical metrics such as fund size, ticket allocation strategy, reserve ratios for follow-on investments, and exit strategy assumptions.

- This exhaustive analysis ensures that only funds with a solid foundation for generating high returns move forward in the evaluation process.

- Diversification-pillar: Isomer places a strong emphasis on ensuring its portfolio remains diversified. This pillar involves evaluating whether a new fund would overlap significantly with existing investments. The objective is to mitigate risks and maximise exposure to diverse opportunities. The strategic decision to decline investment in funds that are too similar to current portfolio members, despite their potential, underscores the disciplined approach to maintaining a balanced and diversified investment portfolio.

- Partnership-pillar: The focus here is on the potential for a mutually beneficial and long-term relationship with the fund managers. Isomer values:

- Open exchange of information and deals, which is crucial for collaborative success.

- The long-term viability of the partnership, considering factors like the fund’s growth trajectory and alignment with Isomer’s investment scope.

- This pillar reflects Isomer’s strategic goal of not just investing in funds but building enduring partnerships that can generate sustained value.

Strategic commitment and team deliberation

After narrowing the field to 12 preferred funds, the Isomer team engages in a comprehensive debate to select three to four funds for investment. This phase involves:

- Strategic alignment and market coverage: Ensuring the chosen funds collectively offer broad market coverage and fit within Isomer’s strategic framework.

- Collaborative decision-making: The selection process is collaborative, reflecting a consensus-driven approach to committing capital. This ensures that decisions are well-rounded and consider multiple perspectives.

Isomer Capital’s methodical approach to fund selection in the Nordic region showcases a blend of strategic foresight, meticulous analysis, and a commitment to building synergistic partnerships. By applying a rigorous set of criteria and engaging in collaborative decision-making, Isomer aims to construct a diversified, high-potential portfolio that aligns with its long-term investment philosophy. This detailed exploration into their methodology underscores the complexities and strategic nuances of venture capital fund selection for LPs, highlighting the importance of fit with the LP’s strategy rather than just the attractiveness of the presented investment opportunity.

Core findings about the Nordic Venture Market

So what learnings does a process like the one above yield for an LP? Aside from facilitating the allocation of new funds, it’s also a cornerstone in the LPs understanding of a geography. Here are the core takeaways from the process left with Isomer on the Nordics.

Learning #1

Micro funds abound in the Nordics, as do the €100m+ funds, but very few €30 to €100 million euro funds exist.

The Nordic VC ecosystem is one of the strongest in Europe, presenting a fascinating tapestry of micro funds and ascending giants:

There were a tonne of micro funds in the Nordics, something that really caught our attention and we’ll be paying close attention to it going forward.

Interestingly, their analysis revealed that there’s a remarkable gap between the micro funds and the large funds with a lot of funds that tipped over the 100 million mark. In the eyes of an LP like Isomer, this insight underlines a unique opportunity spectrum, as this is the sweet spot for their investments.

Learning #2

Finland stands out, and Sweden is very competitive

Looking at the individual markets, the Finnish startup ecosystem stands out as an area of high interest:

For us, one of the things that we always find is that Finland has an amazing ecosystem. It’s super exciting. There’s a lot of great funds there, a lot of activity going on and many funds in target. This is somewhat in contrast to Sweden, where competition is more fierce. But still, Sweden is one of the highest-performing countries, which is incredibly important, of course.

Learning #3

The sustainability funds are very strong

In the Nordics, sustainability has become a driving force with a significant number of breakout funds in the space.

There’s a massive strength around sustainability in the Nordics.

This strength materialises through the rise of climate funds that have taken the stage, ushering in a strong sense of purpose and impact.

This is likely connected to the fact that the funds in the Nordics were some of the very first to turn around and say; “Okay, here is our focused ESG strategy.” Long before sustainability became a buzzword, pioneers in the Nordic countries were already shaping their investment strategies with a keen focus on environmental, social, and governance considerations.

Similarly, the Nordics’ have also shown a dedication to diversity and inclusion, which has enriched the startup ecosystem immensely, fostering collaboration and a tapestry of perspectives.

As the Nordic ecosystem matures, the rise of specialised impact funds is noted:

The Nordic funds have definitely been early leaders in this space. And as the ecosystem continues to develop, we expect to see a lot of impact-led funds and climate funds emerge.

Learning #4

The Nordics are no longer made up of national champions

We’ve definitely gone from having many funds that were nationally focused to many now focusing on “New Nordics” and even some who have gone pan-European.

Indeed, the landscape has evolved with a more insular approach of solely targeting the home country, which is being replaced by a more expansive perspective, which speaks to the maturation of the region’s ecosystem and the foundational premise that tech investing is no national sport.

Founders are not in the business of building businesses to dominate their country. They’re building businesses to build products that can be regional, if not global. As we saw with Angry Birds in the region; they wanted the world to play Angry Birds, not just people in Finland.

Therefore, from what I can see over the last five years or so, everyone has realised that while you may have been focused on your home country and you may have a home-country advantage, you also saw some pretty interesting deals that were on thesis but located in the adjoining countries.

And I think pretty much every fund has told us, ‘Hey, I know that last time we met, we told you we were only focused on Finland, but we’ve done a deal in Gothenberg.

And I can give you examples from every country where they’ve done a deal in another country now. So then they evolve and the next fund comes out and they say, ‘Well, now we’re focused on our home base, but actually we’re putting an office and one or two people in, in the next country over. And that’s a pretty universal story.

There was a time, not very many years ago, where you could do very well by just picking your Swedish fund, your Danish fund, your Finnish fund, and that’s because most firms were just getting started and thus they had a more local thesis that reflected their deal flow.

Register to read more

Please fill in the form to access the full report.